The New Mortgage Market Shift

The New Mortgage Market Shift: When Lenders Stop Being Just Partners and Start Competing for the Buyer

For years, many real estate agents looked at mortgage professionals as one of the most important partners in the transaction. A solid lender could help qualify the buyer, communicate clearly, solve problems early, and most importantly, get the deal to the closing table.

That part has not changed.

But something else is changing.

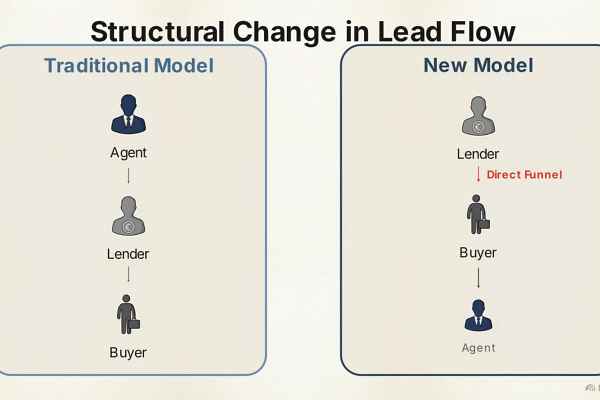

In today’s market, lenders are not only trying to serve buyers. More and more of them are trying to capture buyers directly.

That is the shift.

And if you are a real estate agent, especially one who works heavily with buyers, first-time buyers, or financed deals, this is something worth paying very close attention to.

The mortgage industry is under pressure, and when industries get pressured, they adapt. In this case, many lenders and loan officers appear to be shifting from a relationship-based referral model toward a more aggressive direct-to-consumer model. In plain English, instead of waiting for agents to bring them clients, they are increasingly trying to build their own buyer pipeline through digital marketing, social media, education-based content, paid ads, database marketing, and branded consumer funnels. HousingWire recently highlighted mortgage marketing tactics geared toward helping loan officers attract clients directly while still building referral networks, and National Mortgage News has been discussing growth strategies tied to stronger business development and data-driven lead generation.

That matters because many agents are already dealing with a market where buyers are harder to convert, affordability remains strained, and every lead matters more than it did in easier years.

Why this shift is happening

This did not appear out of nowhere.

The housing market itself is helping create the conditions for it.

According to MBA’s forecast for 2026, total single-family mortgage originations are expected to increase to about $2.2 trillion, with purchase originations forecast to rise 7.7% to $1.46 trillion and refinance originations 9.2% to $737 billion. When lenders see purchase volume opening back up, they naturally compete harder for market share.

At the same time, buyers have more leverage in many parts of the market. Redfin reported on February 23, 2026, that there were an estimated 44% more home sellers than buyers in January 2026, and said the U.S. has effectively been in a buyer’s market by its definition since May 2024. That means the buyers who are active today are especially valuable. Everyone wants them: agents, lenders, portals, lead platforms, and big brands.

There is also a structural shift inside mortgage itself. Independent mortgage banks now originate 84% of all single-family mortgage loans, according to reporting on the CHLA annual report, with even larger shares in FHA and VA lending. That means a huge portion of the market is being driven by aggressive nonbank players who need volume and often move quickly on sales and marketing strategy.

So when you combine:

more competition for fewer active buyers,

pressure on lender margins,

a market where digital branding matters more,

and a purchase market that lenders believe can grow,

you get a more aggressive mortgage marketing environment.

What agents are starting to notice

A lot of agents are seeing the same pattern.

It used to be enough to find a lender who would answer the phone, give a clean preapproval, communicate through underwriting, and get the borrower closed on time.

Now there is another layer.

Agents are asking:

Is this lender really trying to help me serve my client?

Or are they trying to build a direct relationship that eventually cuts me out?

Are they co-marketing with me, or quietly marketing around me?

Are they trying to become the first trusted advisor in the buyer’s mind?

That concern is not paranoia. It is a business reality.

The mortgage industry has leaned harder into educational content, social media visibility, brand-first marketing, automation, and consumer nurture systems. HousingWire’s 2026 mortgage marketing roundup explicitly frames modern loan officer growth around attracting clients, strengthening referral networks, and growing personal brand.

In other words, many lenders are no longer content being “behind the scenes.” They want top-of-funnel visibility.

The social media factor

One big accelerant is social media.

Homebuyers are already searching online for advice, and mortgage professionals know it. Industry coverage in 2025 emphasized that more borrowers are turning to social media for mortgage guidance, and that loan officers have an opportunity to build trust by publishing educational content that feels real and consumer-friendly.

That creates a real opportunity for lenders:

they can teach about credit,

explain down payment assistance,

discuss rate buydowns,

cover preapproval myths,

talk about monthly payment strategy,

and position themselves as the first person a buyer should talk to.

Once that happens, the lender is no longer just part of the transaction. They are part of the lead-generation chain.

And if the buyer starts with the lender, the lender may become the gatekeeper to the agent relationship instead of the other way around.

Why this is especially important after the NAR settlement changes

The post-settlement world changed the way buyers, sellers, and agents talk about compensation. NAR’s settlement practice changes went into effect on August 17, 2024, and buyer representation now has to be discussed more directly and transparently with consumers. NAR’s FAQs also emphasize anti-steering concerns and the importance of proper handling of compensation conversations.

That environment creates space for other industry players to influence consumers earlier.

When buyers are confused about agency, compensation, closing costs, rates, and affordability, whoever educates them first often earns trust first.

That is one reason this lender shift matters so much. Some lenders are realizing that the earlier they enter the consumer conversation, the more influence they may have over the buyer’s decisions, including which agent the buyer ends up working with.

A second trend: lenders are becoming more consumer-facing brands

Another thing worth watching is branding.

Many loan officers used to market mainly to agents, builders, and past clients. Now more are building recognizable public brands. They are running video content, local ads, email campaigns, podcasts, webinars, credit education workshops, first-time buyer funnels, and branded landing pages designed to capture buyers long before an offer is written. Coverage from National Mortgage News and HousingWire reflects this broader emphasis on marketing, technology, and business-development expansion in mortgage.

This means agents are no longer only competing against other agents for online attention. In some cases, they are competing against lenders for the buyer’s trust at the very beginning of the journey.

A third trend: the lead war may change because trigger leads are being restricted

There is another important development here.

For years, one controversial way lenders competed for borrowers was through trigger leads, where a mortgage credit pull could lead to a flood of competing calls and solicitations from other lenders. But new restrictions that took effect on March 5, 2026, sharply limit when consumer reporting agencies can sell trigger leads, generally narrowing outreach to situations involving consent, opt-in prescreening, or qualifying existing relationships.

Why does that matter for agents?

Because if cheap trigger-lead access gets restricted, lenders may shift even more money and attention into:

Google ads,

YouTube ads,

social media,

SEO,

retargeting,

database marketing,

co-branded education,

and direct local branding.

HousingWire reported in February 2026 that mortgage lead prices were rising as trigger-lead restrictions disrupted older lead-generation models and pushed lenders toward costlier online and first-party data channels.

That makes the competition for online buyer attention even more intense.

A fourth trend: compliance risk is rising along with the competition

As lenders and agents look for more creative ways to market together, compliance becomes more important.

Any time mortgage and real estate professionals collaborate on marketing, education, events, lead flow, or value-added services, RESPA concerns have to be taken seriously. NAR’s RESPA resources specifically note that questions around compensation, marketing, and settlement-service promotion require care, and NAR has also advised associations and professionals to consult counsel regarding RESPA compliance when value-added services are involved.

On top of that, the CFPB’s December 2024 case against Rocket Homes and affiliated parties put a spotlight on alleged steering and referral arrangements tied to mortgage and affiliated services. The CFPB later dismissed that case with prejudice in February 2025, but the allegations themselves still reminded the industry how sensitive referral and incentive structures can be under RESPA.

So the new market reality is not just “lenders are advertising harder.”

It is also:

“the more aggressively everyone competes for buyer attention, the more important compliance discipline becomes.”

What this means for real estate agents

This shift does not mean agents should panic.

But it does mean agents should think more strategically.

If lenders are becoming more visible, more branded, and more direct-to-consumer, then agents cannot afford to stay passive in their own marketing.

An agent who depends entirely on referrals from lenders, portals, or random inbound leads may gradually lose ground to professionals who own more of their audience directly.

Here is the uncomfortable truth:

If the lender is educating the buyer first,

capturing the lead first,

following up first,

and building trust first,

then the lender may have more influence over the relationship than the agent does.

That does not mean the lender will always replace the agent. In many cases, they still need a trusted local agent to close the deal well. But it does mean the balance of power can shift.

What strong agents should do now

The answer is not to stop working with lenders.

The answer is to work with the right lenders and build a stronger direct brand yourself.

A few practical takeaways:

1. Choose lenders based on alignment, not just availability.

A responsive lender is still critical. But responsiveness alone is no longer enough. You need to know how they market, how they communicate with consumers, how they handle referral relationships, and whether they see you as a partner or just a distribution channel.

2. Build your own buyer education content.

If lenders are teaching buyers about preapproval, rates, credit, buydowns, and affordability, then agents should be publishing content about contracts, negotiations, market strategy, inspections, neighborhoods, concessions, agency, and how financing choices affect offers. NAR’s research also shows consumers continue to rely heavily on online information and digital behavior in the home search process.

3. Own your database.

Do not let all buyer relationships live inside somebody else’s CRM, ad account, or referral network. Your database is one of your most valuable business assets.

4. Be the local strategist, not just the door opener.

Lenders can explain a payment. They can explain preapproval. Some can explain loan structure very well. But the agent’s role is still powerful when the agent is the person who explains negotiation leverage, pricing behavior, inspection strategy, local inventory shifts, contract risk, and how to actually win in a changing market.

5. Watch the handoff carefully.

If a lender sends you a lead, know how that relationship is being framed. Are you being positioned as the trusted advisor, or as the interchangeable service provider?

6. Keep compliance clean.

The more creative the co-marketing gets, the more important it is to stay within RESPA and brokerage rules. Good intentions do not protect against bad structure.

The opportunity inside the shift

There is actually good news here too.

This market shift creates an opening for agents who are willing to evolve.

Many agents still are not consistently:

publishing content,

building email lists,

explaining agency clearly,

educating buyers early,

or creating systems that keep them top of mind before the mortgage conversation even begins.

The agents who do those things can become stronger, not weaker, in this environment.

In fact, buyer-friendly market conditions may make great agents even more valuable. Redfin’s recent data showing sellers outnumbering buyers means buyers may have more room to negotiate, ask for concessions, and be selective. That kind of environment rewards agents who know how to structure offers and guide financing conversations well.

So yes, lenders may be marketing harder.

Yes, some may be repositioning themselves closer to the consumer.

Yes, the old referral dynamic may be shifting.

But that does not reduce the value of a strong agent.

It increases the importance of becoming one.

Warning Signs an Agent Is Losing Position in the Buyer Relationship

This shift in the mortgage industry is not always obvious at first.

It does not show up as a dramatic change overnight. Instead, it shows up in small signals—subtle changes in how the buyer communicates, who they trust, and who they look to for guidance.

If you pay attention, you can spot it early.

Here are some of the most important warning signs that an agent may be losing position in the buyer relationship:

1. The Lender Becomes the Primary Voice of Authority

If your buyer starts saying things like:

“My lender said this is a good deal…”

“My lender told me to offer this…”

“My lender thinks we should wait…”

That is a shift.

A strong lender should absolutely guide financing decisions. But when they begin influencing offer strategy, negotiation timing, or property decisions, the agent is no longer the primary advisor.

At that point, you are not leading the transaction—you are following it.

2. The Buyer Engages the Lender More Than You

Watch the communication patterns.

If the buyer:

responds faster to the lender than to you

asks the lender more questions than they ask you

updates the lender before updating you

that is a signal.

The person who communicates the most often usually becomes the one the buyer trusts the most.

Consistency builds authority.

3. The Lender Controls the Narrative Around Affordability

There is a difference between explaining a payment and controlling the entire financial narrative.

If the buyer is only hearing:

“Here’s what you qualify for”

“Here’s what your monthly payment will be”

“Here’s how we can structure the loan”

without you adding:

“Here’s what makes sense in this specific market”

“Here’s how this affects your resale”

“Here’s how to negotiate price and concessions”

then the buyer is making decisions based on financing alone, not strategy.

That weakens your role.

4. The Buyer Was “Pre-Sold” Before You Ever Met Them

This is becoming more common.

The buyer:

already has a lender

already trusts that lender

already has a preapproval

already has expectations about price, structure, and timing

before you even step into the picture.

That means you are entering the relationship midstream, not at the beginning.

Whoever meets the buyer first usually frames the conversation.

And whoever frames the conversation often controls it.

5. The Lender’s Brand Is Stronger Than Yours

Take a step back and be honest:

Does your lender have more content online than you?

Are they posting daily on social media?

Are they running ads, videos, and educational content?

Are they showing up when buyers search online?

If a buyer can find your lender everywhere—but cannot easily find you—you are already at a disadvantage.

Visibility builds familiarity.

Familiarity builds trust.

Trust determines influence.

6. You Are Receiving Leads Instead of Owning Relationships

There is nothing wrong with lender referrals.

But there is a difference between:

receiving a lead

andowning the relationship

If your business depends heavily on:

lender referrals

portal leads

third-party sources

then your pipeline is not fully under your control.

And whoever controls the lead source often controls the relationship.

7. The Buyer Quotes the Lender More Than They Quote You

Pay attention to language.

If your buyer says:

“My lender explained this to me…”

“My lender broke this down…”

“My lender showed me how this works…”

but rarely references your guidance, that is a positioning issue.

It means the lender is doing a better job at:

educating

simplifying

communicating

And in today’s market, the best communicator often wins the client’s trust.

8. The Lender Is Introducing You—Instead of You Introducing Them

This is one of the biggest shifts.

Traditionally, the agent introduced the lender.

Now, in some cases, the lender is:

generating the lead

building the relationship

and then introducing the agent

When that happens, the dynamic flips.

You are no longer the quarterback of the deal—you are a recommended service provider inside someone else’s system.

9. You Are Not Involved Early in the Buyer’s Decision-Making

If you are only being brought in when:

it’s time to show homes

it’s time to write an offer

it’s time to negotiate

then you are missing the most important part of the relationship:

the education phase

That is where trust is built.

That is where expectations are set.

That is where loyalty is formed.

And increasingly, that is where lenders are stepping in.

10. Your Follow-Up Is Slower Than Theirs

Speed matters more than ever.

If a lender:

responds faster

follows up more consistently

uses automation more effectively

they will naturally stay top of mind.

Even if you are better at negotiating, advising, and closing deals…

the person who shows up more consistently can still win the relationship.

The Bottom Line

None of these signs, by themselves, mean you have lost the client.

But when multiple of them start to show up at once, it is a clear signal:

The balance of influence is shifting.

And in today’s market, influence is everything.

The agent who:

educates first

communicates best

shows up consistently

and builds trust early

is the one who wins the relationship.

Not the one who shows homes the fastest.

How Agents Take Back Control of the Buyer Relationship (Step-by-Step System)

If lenders are moving closer to the buyer…

then agents need to move earlier, faster, and more strategically.

This is not about fighting lenders.

It’s about owning your position in the relationship before anyone else does.

The agents who win in this market are not the ones who react.

They are the ones who control the flow of the client journey.

Here is the step-by-step system to do exactly that:

Step 1: Become the First Point of Contact (Top-of-Funnel Control)

The first conversation wins.

Whoever meets the buyer first:

frames expectations

builds trust

sets the process

and defines their role

If that is the lender, you are already playing catch-up.

If that is you, you control the relationship.

What to do:

Create simple content that answers buyer questions:

“How much do I really need to buy a home?”

“What does my monthly payment actually include?”

“What should I do before talking to a lender?”

Use:

YouTube (long-form education)

Shorts/Reels (quick hooks)

Email/newsletter (nurture)

Landing pages inside your CRM

Give buyers a reason to come to you first, not after they’ve already been pre-sold.

👉 Your goal is simple:

Be the first trusted advisor—not the last piece of the process.

Step 2: Control the Education Phase (Position Yourself as the Strategist)

Most agents skip this.

Most lenders don’t.

That is why lenders are gaining ground.

If you do not educate your buyer early, someone else will.

What to do:

Create a simple “Buyer Clarity Framework” you walk every client through:

Financing basics (in partnership with lender)

Market conditions (local + real)

Offer strategy

Negotiation expectations

Inspection mindset

Closing cost strategy (including concessions)

You are not replacing the lender.

You are expanding the conversation beyond just the payment.

👉 Positioning shift:

From “agent who shows homes” → “advisor who builds the entire plan”

Step 3: Introduce the Lender (Don’t Be Introduced)

This is critical.

The moment the lender introduces you instead of the other way around,

you have lost primary position.

What to do:

Build a shortlist of 2–3 vetted lenders

Explain to your buyer:

“I’ve worked with several lenders. These are the ones I trust to actually get deals closed.”

Frame it as protection, not control

This positions you as:

the gatekeeper of quality

the protector of the transaction

the one managing the team

👉 You are the quarterback. Not a referral partner.

Step 4: Own the Communication Rhythm

Whoever communicates the most consistently wins trust.

Not the smartest. Not the most experienced.

The most consistent.

What to do:

Set a communication standard:

Weekly check-ins (even if nothing changed)

Clear next steps after every conversation

Recap messages after major discussions

“Here’s what happens next” guidance

Use your CRM to:

automate follow-ups

send milestone updates

stay top-of-mind

👉 Consistency beats charisma in long-term trust.

Step 5: Build Your Own Database (Stop Renting Your Business)

If your business depends on:

lender referrals

Zillow/Realtor leads

third-party systems

you do not own your pipeline.

What to do:

Capture every lead into your CRM

Build:

email lists

text nurture campaigns

retargeting audiences

Send:

market updates

buyer tips

deal breakdowns

local insights

👉 Your database is your business. Everything else is temporary.

Step 6: Create Content That Lenders Don’t Cover

Lenders are great at:

payments

rates

loan programs

They are not built to dominate:

negotiation strategy

local market insight

property analysis

contract protection

That is your lane.

Content ideas:

“How to win in a multiple-offer situation”

“How to negotiate repairs and concessions”

“What agents look for that buyers miss”

“How to avoid overpaying in today’s market”

👉 Own the strategy conversation, not just the transaction.

Step 7: Control the Offer Strategy Conversation

This is where agents either win or lose their authority.

If the buyer is asking the lender:

“What should I offer?”

“Should I go higher?”

“Can I ask for concessions?”

you are losing ground.

What to do:

Take ownership of:

pricing strategy

offer structure

risk tolerance

negotiation approach

Work with the lender—but do not defer to them.

👉 The lender supports the deal. You structure it.

Step 8: Build a “Team Experience,” Not a Hand-Off

Instead of:

👉 “Here’s my lender, go talk to them”

You say:

👉 “We’re going to work as a team to get you to the closing table”

Then:

stay involved in financing conversations

align messaging with the lender

ensure the buyer sees you as the lead advisor

👉 You are not passing the client—you are managing the team.

Step 9: Use Systems to Stay Top of Mind (Even When You’re Busy)

The reality is simple:

If your lender has:

better follow-up

better automation

better consistency

they will win attention.

What to do:

Inside your CRM:

Create:

Buyer nurture sequences

Weekly value emails

Check-in automations

Tag buyers by stage:

New lead

Pre-approved

Shopping

Under contract

Long-term nurture

👉 Automation does not replace relationships—it protects them.

Step 10: Build a Personal Brand That Outlives Any Deal

This is the long game.

The strongest agents are not just service providers.

They are known names in their market.

When buyers:

recognize you

trust your content

feel like they already know you

you win before the first conversation.

What to do:

Post consistently (YouTube, Facebook, Instagram)

Share real insights—not just listings

Be the voice of your market

👉 If your brand is stronger than your lender’s, the relationship stays yours.

The Real Strategy

This is not about competing with lenders.

It is about leading the client journey.

The best agents:

collaborate with strong lenders

respect their expertise

and still maintain control of the relationship

Because at the end of the day:

👉 The lender finances the deal

👉 The agent guides the decision

And in today’s market, the person who guides the decision

is the one who owns the relationship.

Final thought

The mortgage professional who answers the phone, keeps the loan moving, and gets the client to the closing table is still incredibly valuable.

But in today’s market, agents may need to ask a new question:

Is this lender only helping me close business, or are they also building a system that competes with me for the client relationship?

That is the real shift.

And the agents who recognize it early will be in a much better position to adapt, protect their pipeline, and build a business that does not depend on somebody else controlling access to the buyer.

If you still have question feel free to reach out James Smith (281)825-4880